Due to the current “social distancing” and other measures in place to control the COVID-19 outbreak in Australia, a significant portion of the workforce has been required to work from home. As this has meant many employees are incurring more than usual home office expenditure, shouldn’t they then be eligible to claim this as a tax deduction?

Home office expenses and tax deductions

Prior to 1 March 2020, there were two options available to employees to claim their home office expenses as a tax deduction; the actual cost method, or the fixed rate per hour method. Due to the large influx of employees moving to work from home arrangements, the ATO recently announced a new shortcut method that applies from 1 March 2020 to 30 June 2020.

General rules

Similar to any other employment related expenses, tax deductions can only be claimed for home office expenses to extent that the following principles have been satisfied:

- The expenses must have been incurred by you;

- The expenses have not been reimbursed by your employer;

- The expenses must be in relation to your income earning activity; and

- You must have a record as evidence.

What expenses can be claimed

Examples of running costs that can be claimed as a tax deduction include:

- Additional electricity costs in relation to heating, cooling, lighting and cleaning your home as a result of working from home;

- Work related phone and internet expenses;

- Ink, printer paper and stationery used for work; and

- Decline in value of home office equipment such as computers, printers, phones, furniture and furnishings.

You cannot claim a tax deduction occupancy expenses such as interest on mortgages, rent and council rates. The exception to this general principle is if you have a dedicated area for a workplace. For example, a hairdressing business that is run at home where there is a dedicated area to perform the services, such as cutting and washing hair or a doctor that maintains a consulting room in their home. Extra care should be taken if you are considering claiming occupancy costs as these can limit the ability to apply any main residence exemption to the ultimate sale of your home.

Actual cost method

The actual cost method allows individuals to claim the actual running costs of their home office provided they can evidence the deductible proportion of the total expense incurred. This evidence generally needs to be in the form of itemised invoices specifying the deductible proportion of a taxpayer’s usage for each period to support the annual deduction. As this can be difficult to ascertain, particularly in relation to the allocation of utility expenses, the ATO allow taxpayers to estimate these costs provided that the estimate is based upon a representative 4 week period and that the usage is constant throughout the entire year, e.g. if an individual works from home 1 day every week they will be eligible to claim 20% of their actual utility usage costs. If a taxpayer is seeking to utilise this method, it should be noted that no claim can be made if the taxpayer does not have an appropriate representative period.

In addition to utility expenses, deductions are also allowable for the depreciation related to the purchase of computers, desks, chairs, monitors, computer accessories, telephones, etc. It is easier to support the actual usage of such costs; however, any use of these items by other members of the household can limit a taxpayer claim.

Where the cost of these assets is less than $300, the taxable use percentage can be claimed in the year in which it was acquired. If the asset cost is more than $300 it must be depreciated over its useful life and only the taxable use percentage of the depreciation expense can be claimed.

Fixed-rate method

As the actual cost method is difficult for most taxpayers to manage (and many taxpayers do not work from home on a consistent or regular basis and do not have a representative period), the ATO have provided a fixed rate method to assist them in claiming deductions for running their home office.

The fixed-rate method allows taxpayers to claim deductions for the following:

- Rate of 52 cents per hour on running expenses, such as heating, cooling, lighting cleaning and decline in value of office furniture (e.g. office chair & desk).

- Actual work-related usage costs related to phone, internet, ink, printer paper, and stationery; and

- Actual work-related costs of the purchase and/or decline in value of home office equipment (e.g. computer, monitor, printer and phone).

To support taxpayers that might not wish to make a claim for the actual usage of their phone or internet, the ATO allow a fixed amount of $50 as a deduction with no substantiation required.

Shortcut method (from 1 March 2020 to 30 June 2020)

Due to the recent requirement for many Australians to work from home due to the COVID-19 outbreak, the ATO have provided a new shortcut rate of 80 cents per hour on additional running expenses incurred from 1 March 2020. As this rate is intended to cover all work related home office costs including phone, internet, ink, printer paper, and decline in value home office furniture & equipment, no further deduction can be claimed for any of these items in addition to the per hour allowance if the shortcut method is used from 1 March 2020. Importantly, this method only applies to those who:

- Are working from home or running their business. However, this does not include those who are on leave or have been stood down, or in the case of running a business, have stopped operating permanently.

- Note: Working from home does not include minimal tasks such as checking emails or taking calls; and

- Have incurred additional expenses as a result of working from home due to COVID-19.

Deductions can only be claimed under the shortcut method for the period 1 March 2020 through 30 June 2020, and taxpayers must keep a record of the hours that they have worked from home. Taxpayers wishing to claim a deduction using this shortcut method must include a specific ‘COVID-hourly rate’ narration next to the deduction in their tax return.

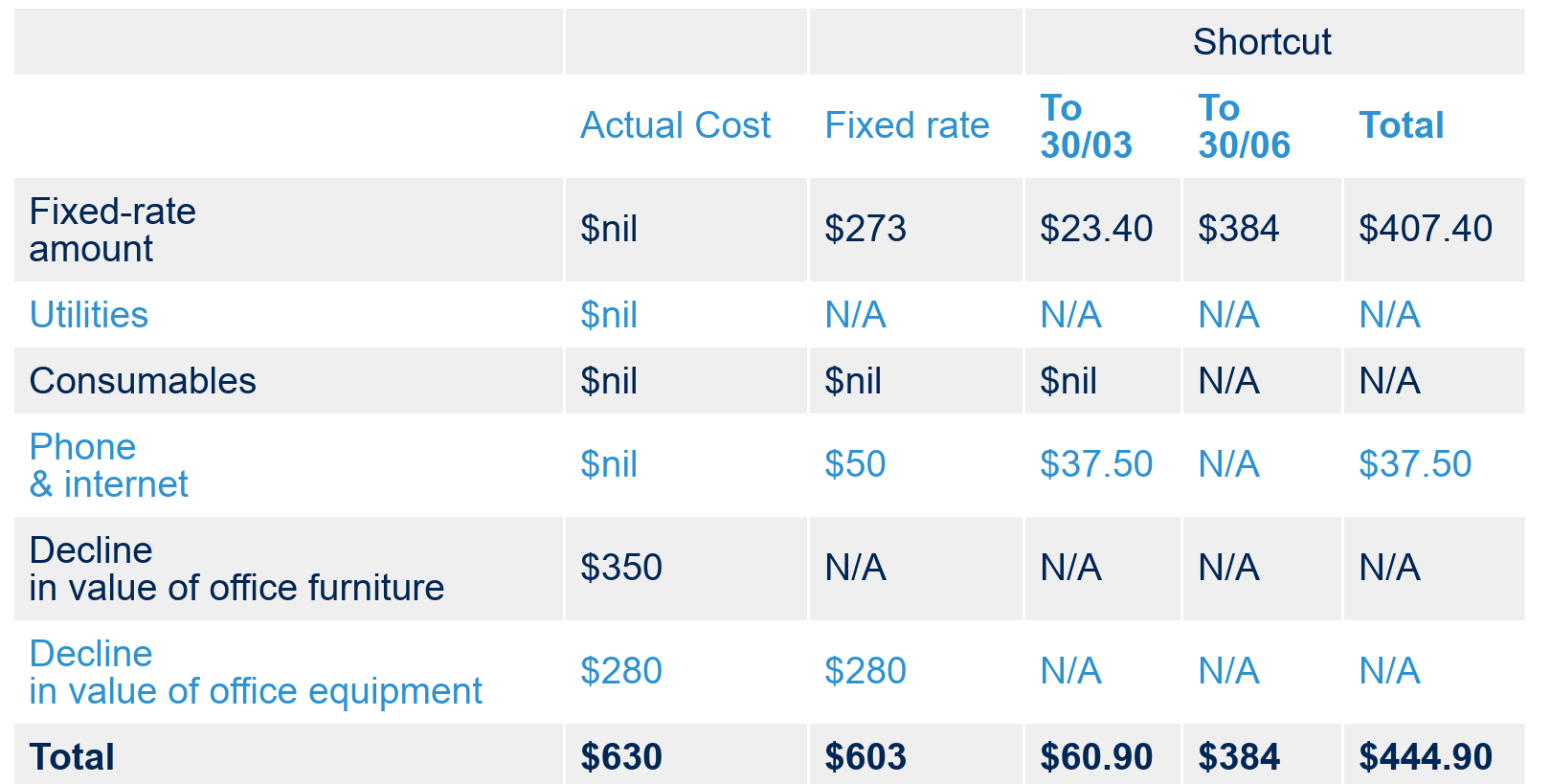

Worked example

Jane Smith, a Chartered Accountant, resides in St Kilda and ordinarily works from her office in the CBD of Melbourne. While Jane does not have a dedicated workspace at home, she does work from home ad-hoc as this suits her needs. As this is the case, Jane determines that she has no comparison period that she can use to claim utility expenses. Jane also does not maintain records related to the business use of her phone.

Due to the current COVID-19 outbreak Jane has been requested to work from home full-time from 30 March 2020 for the foreseeable future. As a result of being required to work from home, and after deciding that the kitchen table is not suitable for full-time work, on 4 April 2020 Jane purchases a new office chair for $100, a new desk for $250 and a new monitor for $280 for her to use at home. She retains these receipts, specifying that these are 100% used for a taxable purpose, and maintains comprehensive timesheets of the hours she works up to 30 June 2020. She has determined that she has worked at home for 480 hours between 30 March and 30 June 2020. Prior to 30 March her timesheets indicate that she worked from home a total of 45 hours and she had not spent any days in March working from home.

As Jane does not have a comparison period upon which to base her utility usage deduction, she is unable to claim any amount in relation to these costs using the actual cost method. Similarly, as she does not maintain comprehensive records regarding the business use of her phone, she is not able to claim a deduction using the actual cost method. As she has receipts specifying the taxable use percentage of the assets she acquired, she can claim these costs in the year in which they were incurred.

Given that Jane is unable to claim costs associated with working from home using the actual method, she has calculated the costs of maintaining her home office using the fixed-rate and shortcut methods.

Under the fixed-rate method, Jane is able to claim a deduction of $0.52 for the 525hrs worked at home, plus $50 for phone and internet usage. In addition, as the fixed-rate method does not allow for the decline in value of office equipment (such as computers or other peripheral devices), she is able to claim the cost of the new monitor of $280. As the fixed-rate method does incorporate the decline in value of office furniture, no deduction is available in relation to the new desk or chair.

Under the shortcut method, Jane is able to claim $0.52 for the 45 hours worked at home between 1 July 2019 and 29 February 2020, plus $0.80 for the 480 hours worked at home between 30 March 2020 and 30 June 2020. As the shortcut method allows for the cost of the use of phone and internet as well as the decline in value of all assets, she is unable to claim additional expenses for these costs. While she is unable to claim these additional costs while she is using the shortcut method, she is entitled to claim a portion of any such expenses for the 9 month period to 30 March 2020 (i.e. in this case, a portion of the $50 phone and internet amount).

Based on the above information, Jane’s potential income tax deductions under each method are set out below:

As can be seen above, whilst the shortcut method is the easiest to apply, the actual cost and fixed-rate methods would yield a higher tax deduction for Jane.

In summary

While individual taxpayers can choose from three methods to claim deductions for expenses incurred while working from home, particular care should be taken in determining the appropriate method based upon the level of documentation they hold. Individuals should also ensure that they “run the numbers” to see if the new shortcut rate announced by the ATO is indeed as good as people assume it is.

Conclusion

For a confidential discussion related to your available personal income tax deductions, please reach out to one of our Fordham Partners.

If you have any queries, or would like to discuss the above further, please contact your Fordham Partner.